AKG weekly charts - Issue #110

AKG weekly charts - Issue #110

FC August 2023 newsletter - Paring down of Portfolio risk (read here)

Summary of financial markets in last week here

[1] The bond market is telling the Fed it's done with rate hikes. There's just a 15% chance of a September rate hike being priced into fed funds futures, and a 21% chance of one in November. The Fed is now expected to start cutting rates in early 2024, according to market pricing.

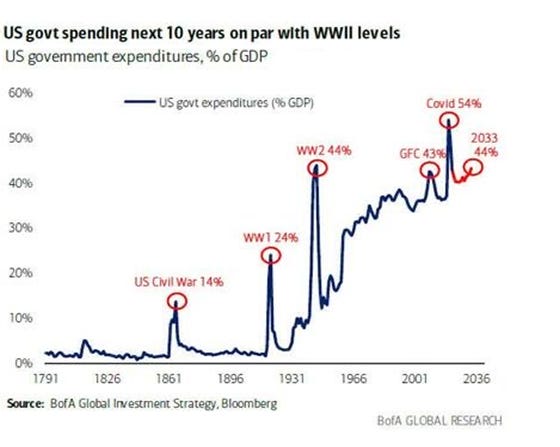

[2] The expected US government spending over the next 10 years will results in tax hikes and this could set up dangerous levels of debt for fiscal space to be compromised. Wait and watch!

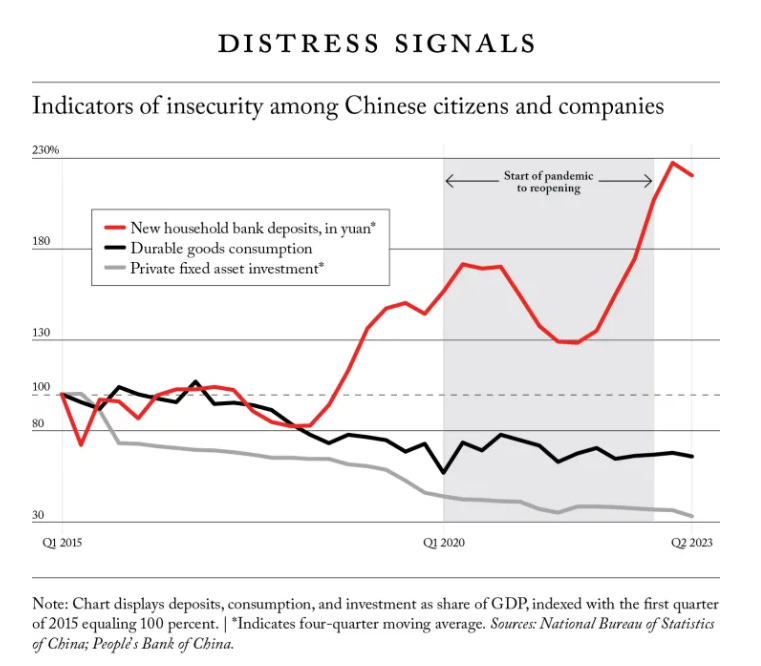

[3] China is suffering from "long economic Covid"

"Like a patient suffering from that chronic condition, China’s body economic has not regained its vitality and remains sluggish even now that the acute phase...has ended."

Read more here by Adam Posen.

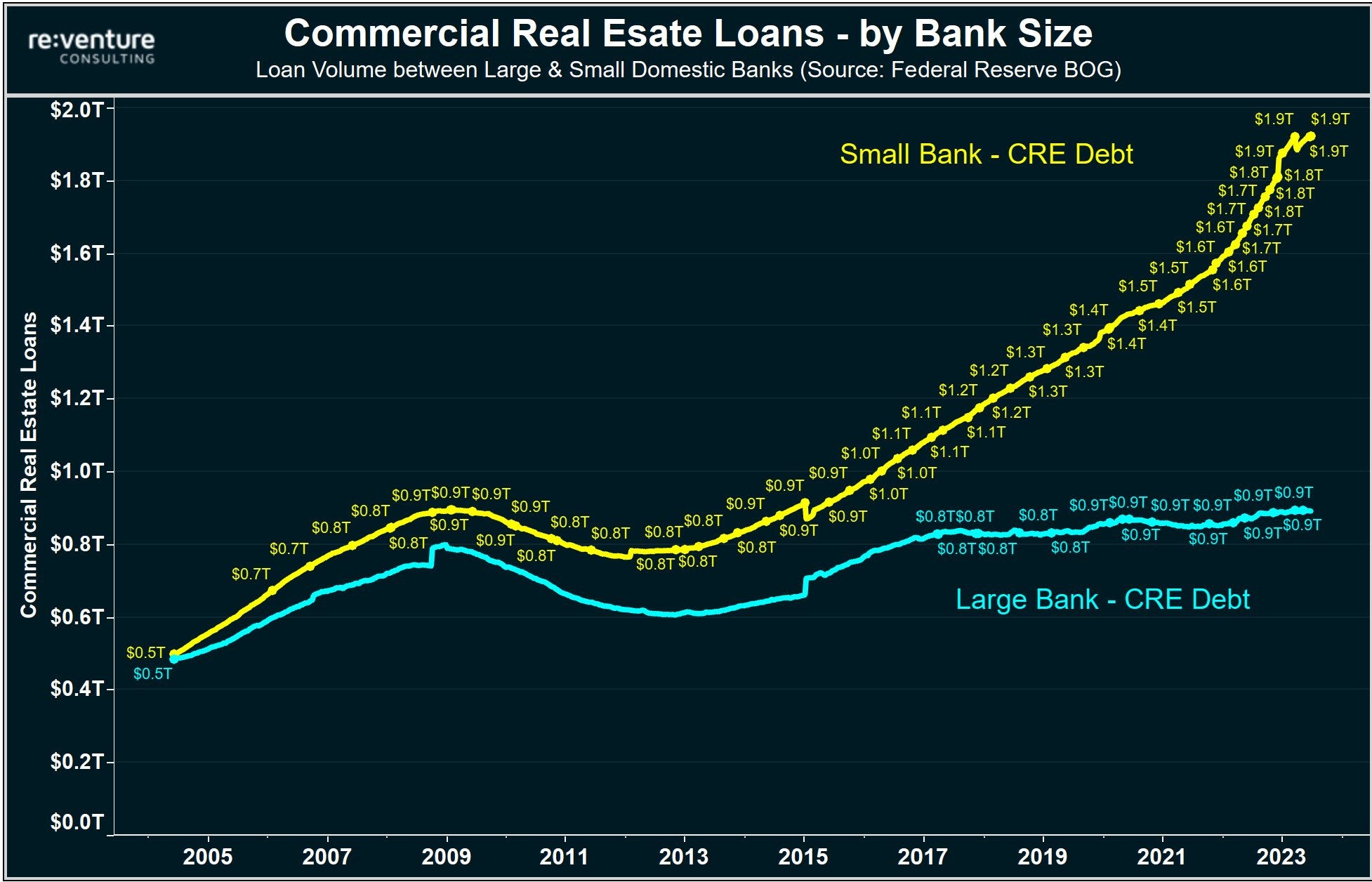

[4] Small banks now hold a massive $1.9 Trn of commercial real estate (CRE) loans in US. This is up nearly $1 trillion since 2017 while large bank exposure stood flat. CRE is also dealing with mass vacancies and prices are down 20%+ in 1 year. The worst part?

Over $1.5 trillion of CRE loans are due to be refinanced by 2025. Many of these loans have seen rates nearly double. Higher rates, falling prices and mass vacancies. All with record levels of exposure to the same banks that almost collapsed this year. What could possibly go wrong?

h/t @KobeissiLetter

[5] Italian banks slump after govt introduces windfall tax. Deputy PM Salvini announced a 40% levy on extra profits of lenders for 2023 as part of a wide-ranging decree approved at a cabinet meeting. Analysts estimate it will wipe 19% from bank earnings.

Connect on various social media platforms here

Subscribe to (free) AKG weekend readings newsletter here

Follow #FCOTTReco and #FCBookReco on our Twitter page here.

[6] Investors appear to be increasing their investments towards Alternative Investment Funds (AIF) over the years. A reflection of improved risk-apetite or taking advantage of tax-breaks?

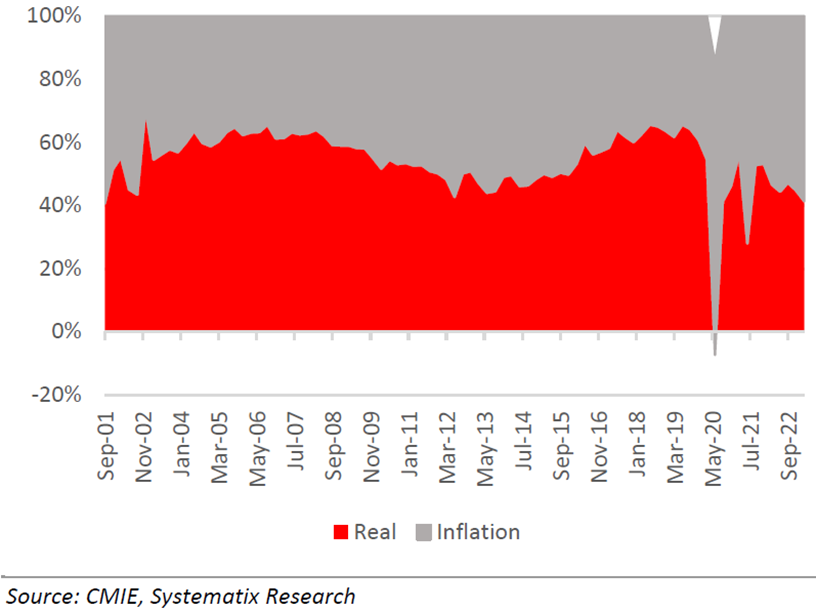

[7] Nearly 60% of nominal GDP spending in India appears be inflation, much higher than pre-Covid levels. The K-shaped recovery just got real!

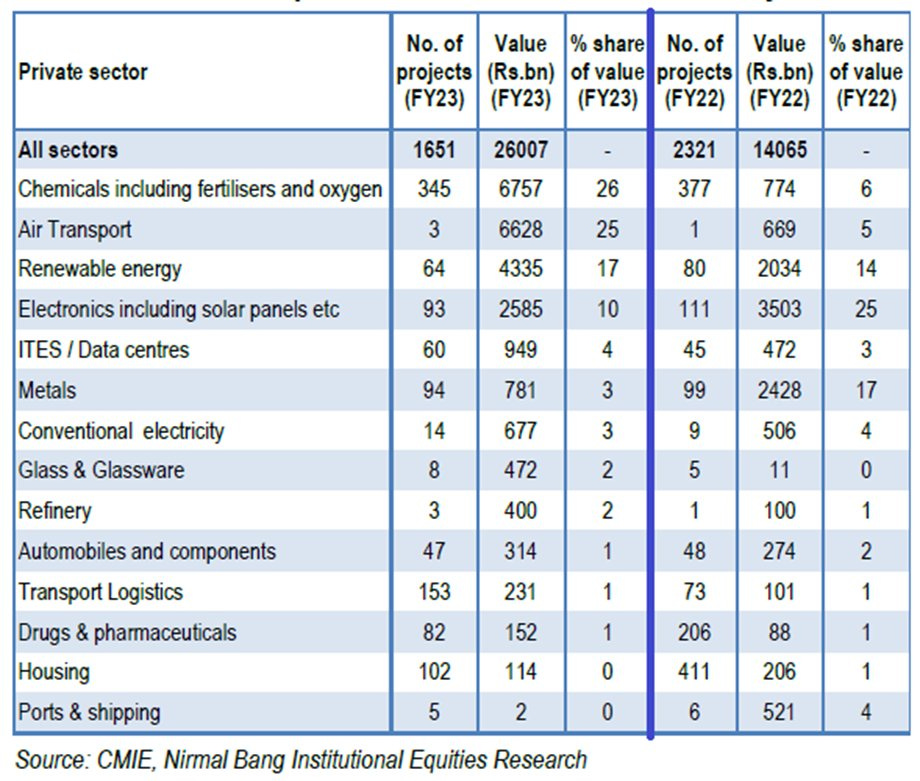

[8] Capex announcements in FY23 have been led by chemical and air transport - two spaces where Fintrekk capital subscribers are invested. (see here for our equity products)

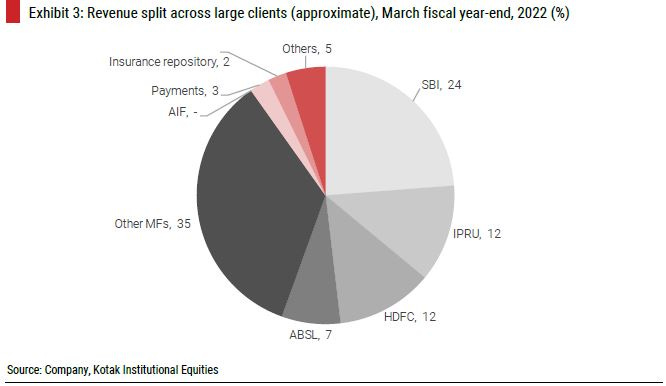

[9] CAMS has high revenue concentration among its large AMC clients. With 2 new licenses approval coming from SEBI in last week, CAMS will be a beneficiary.

Disclosure : No positions, only a view.

[10] The rail transport has been seeing serious ramp-up in the post Covid phase for dispatching vehicles with 18% vehicles in FY23 as compared to FY20, a rise of 50

Disclaimer:

This newsletter is for information and educational purposes only. In this material, Amit Kumar Gupta (SEBI registered Research Analyst, INH100009327) has used information that is publicly available and is believed to be from reliable sources. While utmost care has been exercised, the author does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers, before acting on any information herein should make their own investigation & seek appropriate professional advice. Any sector(s)/ stock(s)/ issuer(s) mentioned do not constitute any recommendation and the RA may or may not have any future or existing position in these. All opinions/ figures/ charts/ graphs are as on date of publishing (or as at mentioned date) and are subject to change without notice. Any logos used may be trademarks™ or registered® trademarks of their respective holders, our usage does not imply any affiliation with or endorsement by them. Past performance on charts may or may not be sustained in the future and should not be used as a basis for comparison to infer any investment ideas