AKG weekly charts - Issue #127

AKG weekly charts - Issue #127

This newsletter is a weekly selection of 10 charts hand-picked across the internet which pertains to our investment strategy and bring an updated insight and perspective.

Connect on various social media platforms here

Subscribe (free) to #AKGweekendreadings here [released every Friday evening]

[1] Based on historical movements, time for Bitcoin to catch up with NASDAQ rally. Disc : I am bullish Bitcoin.

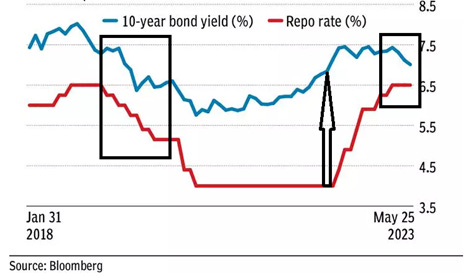

[2] Interest rates (and bond prices) are a function of the demand and supply of credit. RBI policy rates do provide a broader direction to the credit demand and supply, but it is not necessary that in the near-term RBI rates and bond prices will have a direct correlation. The biggest misconception floating around at this time!

[3] The US interest expense is more than 1trn$ now. If there is a country which can’t afford any more rate hikes and would love some rate cuts, it is US

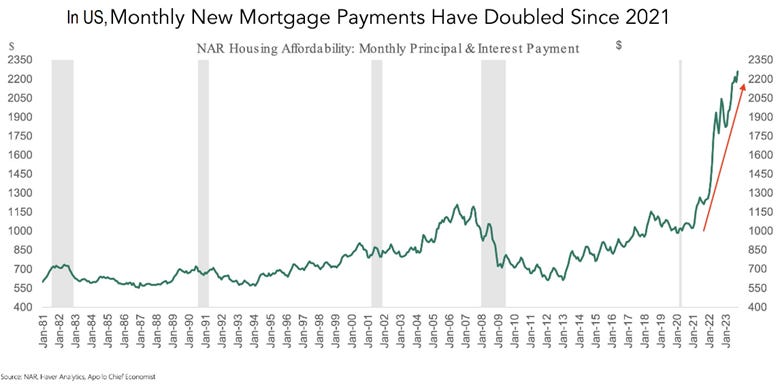

[4] Not many know that US mortgage rates have stopped rising since Oct 2022 but mortgage payments have doubled since 2021. The last few rate hikes by Fed had no impact, so will the first few rate cuts in 2024 (unless happens overnight)

[5] China’s trade surplus with proxy countries (countries used by many countries to indirectly import from China) has increased meaningfully, implying some rerouting of trade. China+1 is a lot of smoke!

[6] The US money supply is undergoing a contraction in M2. Recession-like conditions to follow in H2CY2024?

[7] Unlike manufactured goods, the first stage of production of commodities depends on natural endowments that can be concentrated geographically.

As a result of natural endowments’ concentration, there is a significant concentration of production at the country level, with the top three producers accounting on average for about 65% of the global output of agriculture, about 50% of energy, and about 75% of minerals commodities.

[8] India ranks second in Asia on Supply Chain relocation

Source: UBS

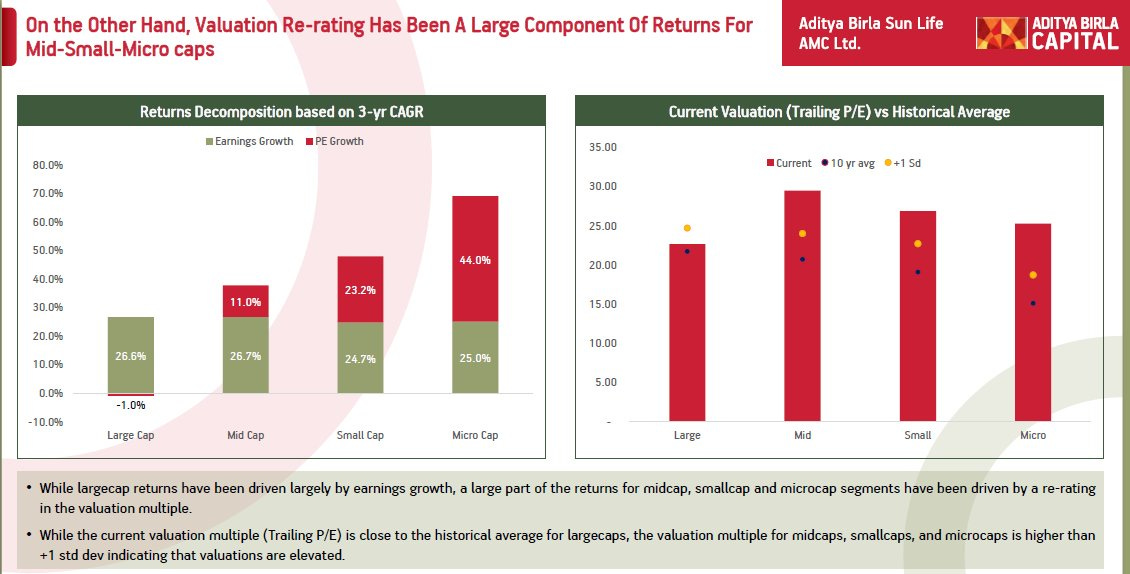

[9] Re-rating for large caps is a larger probability than re-rating in SMID and micro-cap space at an index level.

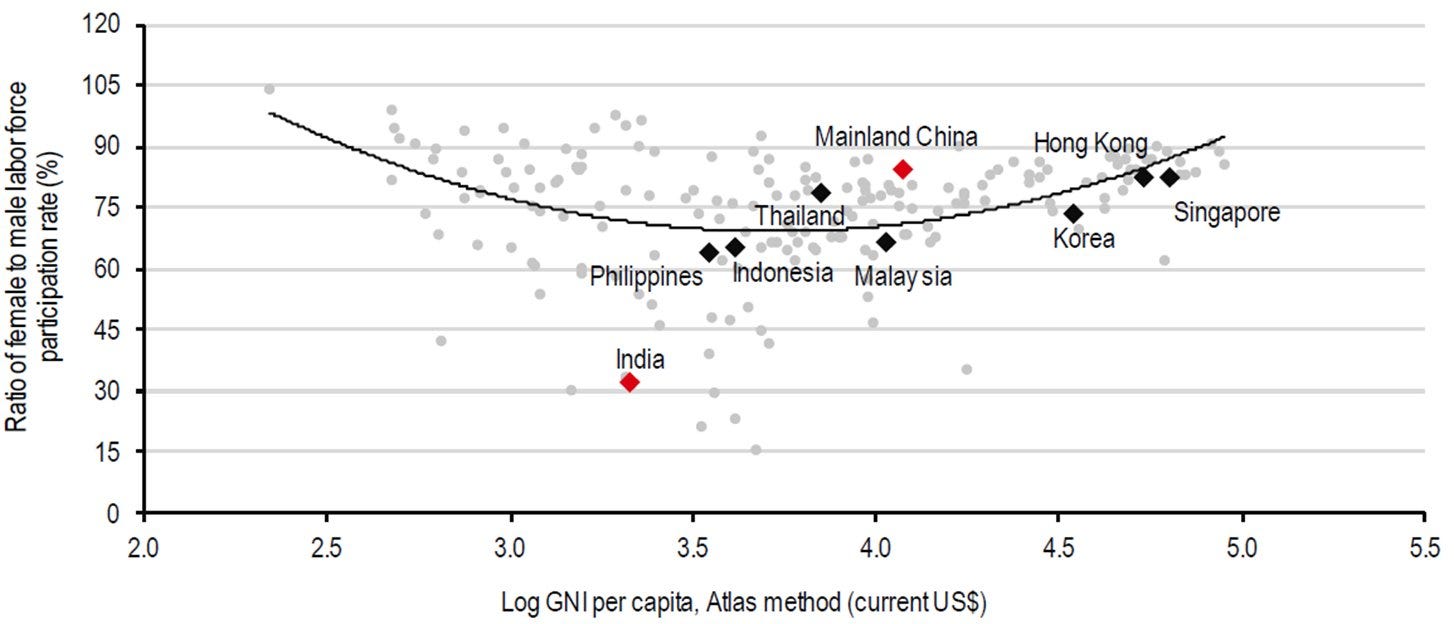

[10] Even though things have improved in the last decade, a shift up in India’s female labour force would bring about a significant change in both labour supply and cost dynamics for companies.

Source: HSBC

Disclaimer:

This newsletter is for information and educational purposes only. In this material, Amit Kumar Gupta (SEBI registered Research Analyst, INH100009327) has used information that is publicly available and is believed to be from reliable sources. While utmost care has been exercised, the author does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers, before acting on any information herein should make their own investigation & seek appropriate professional advice. Any sector(s)/ stock(s)/ issuer(s) mentioned do not constitute any recommendation and the RA may or may not have any future or existing position in these. All opinions/ figures/ charts/ graphs are as on date of publishing (or as at mentioned date) and are subject to change without notice. Any logos used may be trademarks™ or registered® trademarks of their respective holders, our usage does not imply any affiliation with or endorsement by them. Past performance on charts may or may not be sustained in the future and should not be used as a basis for comparison to infer any investment ideas