AKG weekly charts - Issue #132

AKG weekly charts - Issue #132

This newsletter is a weekly selection of 10 charts hand-picked across the internet which pertains to our investment strategy and bring an updated insight and perspective.

Summary of financial markets in last week here.

Connect on various social media platforms here

Subscribe (free) to #AKGweekendreadings here [released every Friday evening]

Feb’24 review of our equity research strategies - Emerging leaders & Special Situation

[1] Though Government has doled out PLI for ACC and placed emphasis on domestic value addition, the cell component players too are looking forward to incentives. Reducing dependence on lithium resources and developing low-cost battery systems is driving research on sodium-ion batteries (Na). Though Na batteries show greater promise due to abundance of availability and low cost, energy density remains a concern.

[2] For every $1GDP growth, US utilizes $2.5 in debt. How long this fiscal can sustain in high interest rate regime?

[3] The Union health secretary has been asked to convene a meeting with the health secretaries of all states to ensure that standard rates are notified within a month. If Union govt fails to find a solution, then it will consider petitioner's plea for implementing CGHS-prescribed standardized rates. 12-60% price differences for various procedures currently. [Media quote in Business standard here]

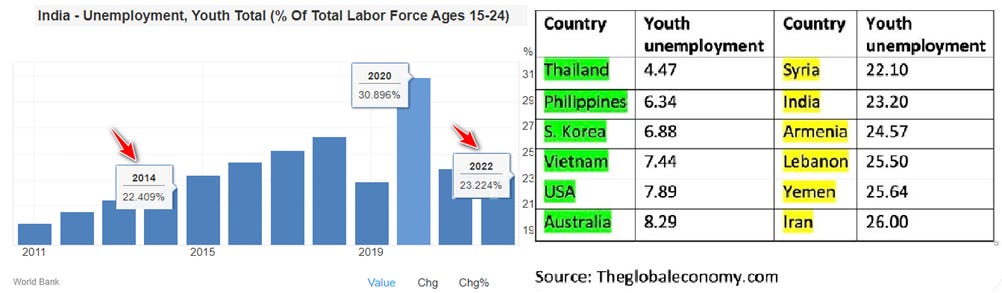

[4] India faces one of the worst youth unemployment rates globally. Indian homemakers are facing serious challenges in managing their household budgets due to inflation. According to the World Bank, the youth unemployment rate in India could be comparable to war-torn economies like Syria, Yemen, Lebanon etc. The unemployment rate and household inflation have worsened or failed to improve in the past 10 years.

[5] The brokerage industry is having a “remove wheat from chaff” moment. Number of users gained for the top brokers is directly proportional (approx) to the number of users lost by the bank/NBFC led brokers.

[6] Mumbai and Delhi airports cumulately handle 11cr footfall. Aviation is a decadal theme in India!

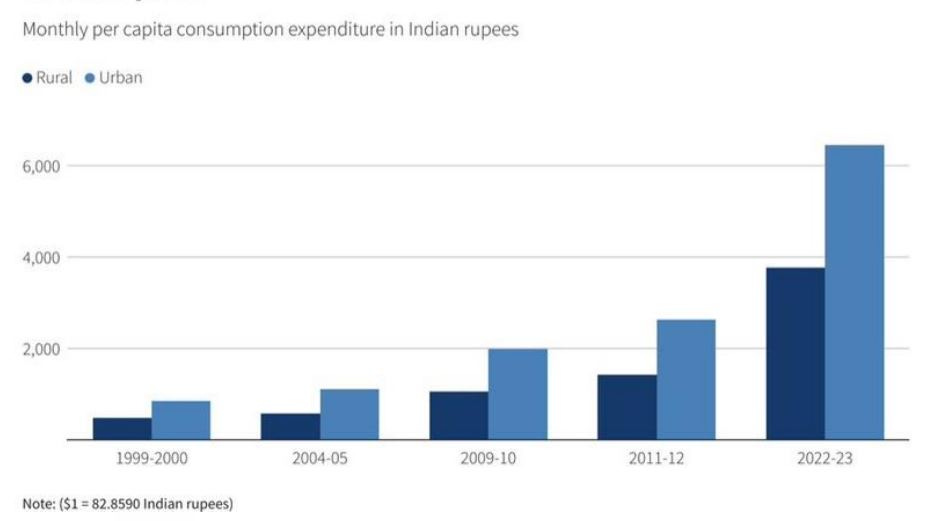

[7] Rural and Urban divide in consumption expenditure has widened in post Covid world as indicated by the recent wealth surveys. K-shaped recovery continues.

[8] Despite all the EV and clean energy euphoria in Indian markets, world oil demand is having a “break-out” moment.

[9] While most of us have heard about the magnificent 7 in the US stock markets, how many have heard about the magnificent 3 in Europe?

These magnificent 3 accounted for all of the returns of Stoxx 600:

- ASML

- Novo Nordisk

- SAP

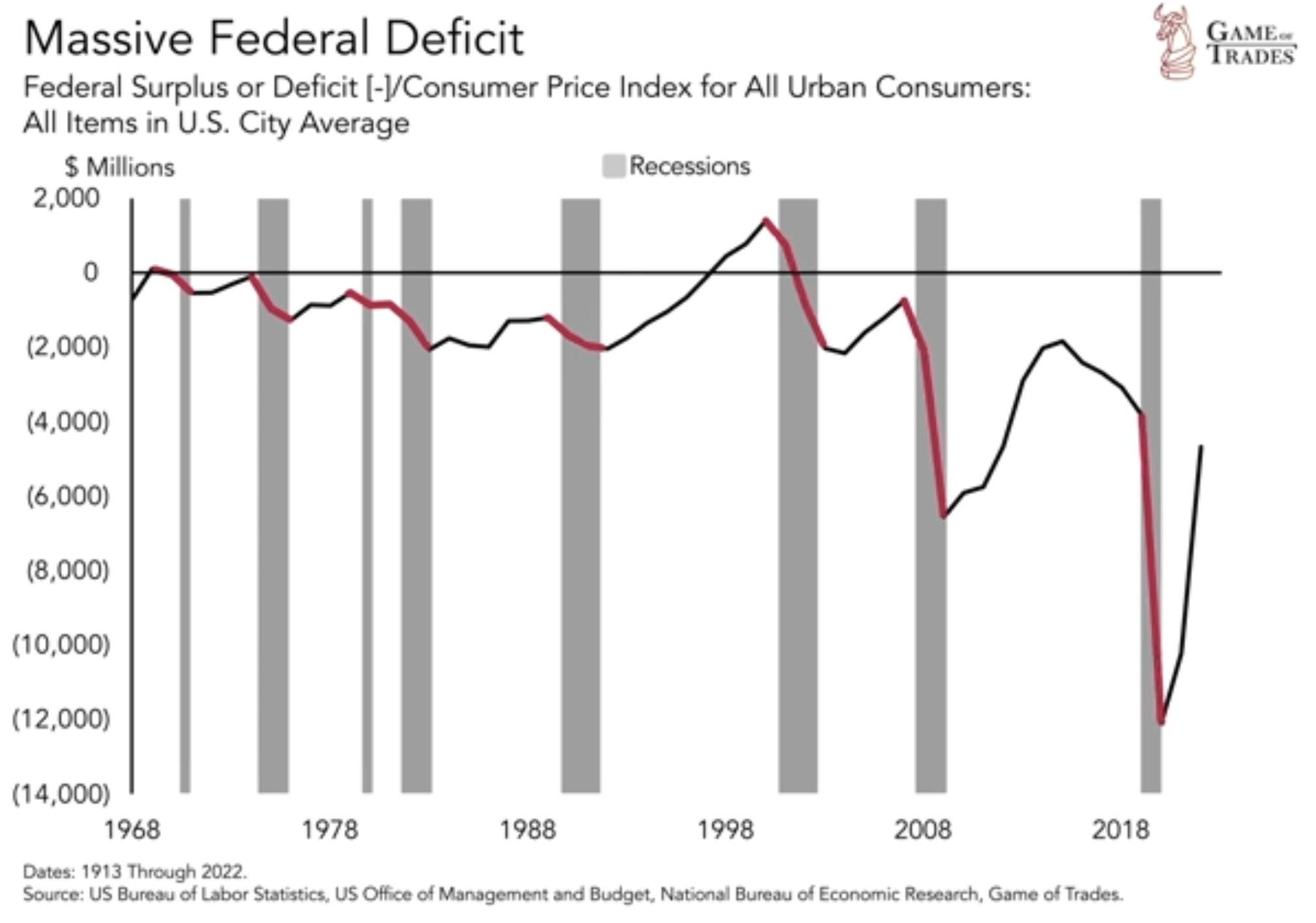

[10] Recessions typically lead to more federal deficit but the debt bubble cannot go on forever in US. Timing is tough to predict.

Disclaimer:

This newsletter is for information and educational purposes only. In this material, Amit Kumar Gupta (SEBI registered Research Analyst, INH100009327) has used information that is publicly available and is believed to be from reliable sources. While utmost care has been exercised, the author does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers, before acting on any information herein should make their own investigation & seek appropriate professional advice. Any sector(s)/ stock(s)/ issuer(s) mentioned do not constitute any recommendation and the RA may or may not have any future or existing position in these. All opinions/ figures/ charts/ graphs are as on date of publishing (or as at mentioned date) and are subject to change without notice. Any logos used may be trademarks™ or registered® trademarks of their respective holders, our usage does not imply any affiliation with or endorsement by them. Past performance on charts may or may not be sustained in the future and should not be used as a basis for comparison to infer any investment ideas