AKG weekly charts - Issue #159

This newsletter is a weekly selection of 10 charts hand-picked across the internet and research reports which pertains to our investment strategy and bring an updated insight and perspective

Aug’25 review of FC equity research strategies- Emerging leaders, Special Situation & Wealth Compounders. [Visit www.fintrekkcapital.com for subscription details]

Connect on various social media platforms here

Subscribe (free) to #AKGweekendreadings here [Newletter released every Friday]

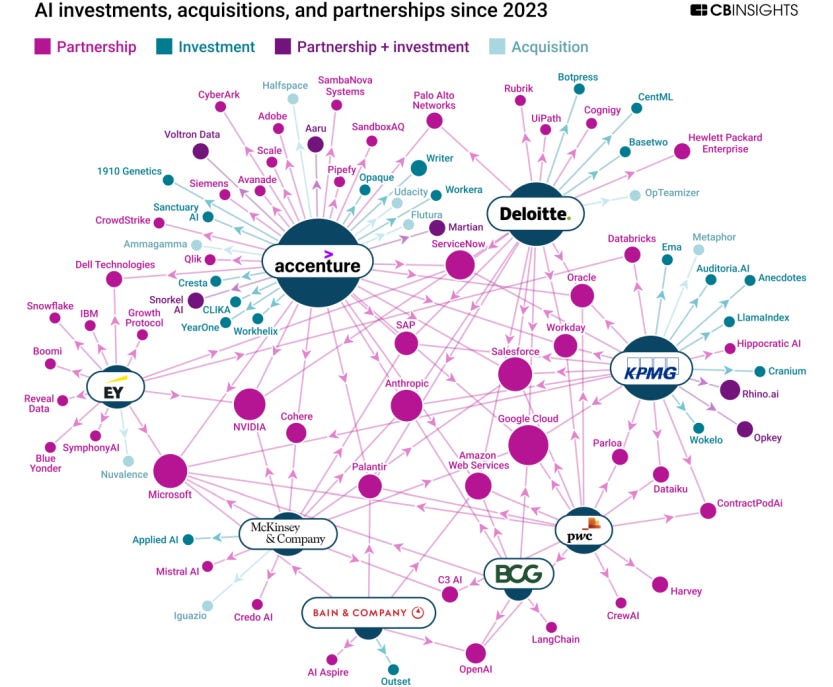

[1] How professional services firms are building their Al agent strategies…

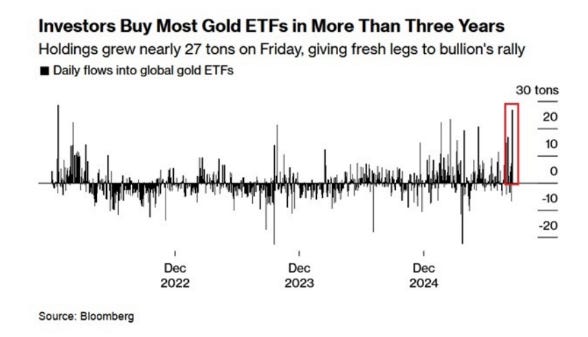

[2] Momentum buyers pushing the inflows in Gold ETFs amid Fed rate cuts…

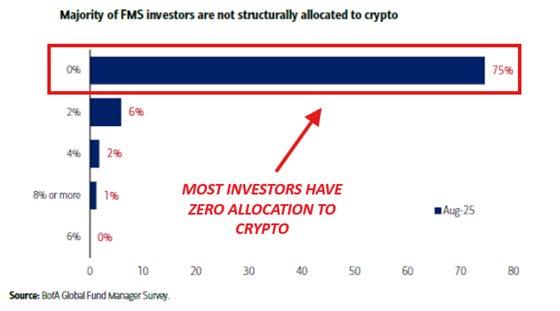

[3] Instiutions are under-allocated in Crypto. It’s mostly led by retail and household investors…

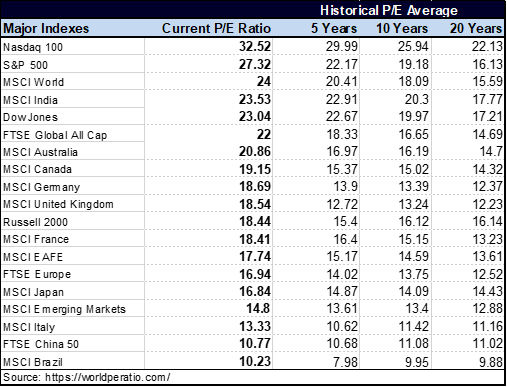

[4] A consistent rise in global equity prices, not accompanied by a matching earnings growth, has raised concerns about the sustainability of current valuations [See full note here]

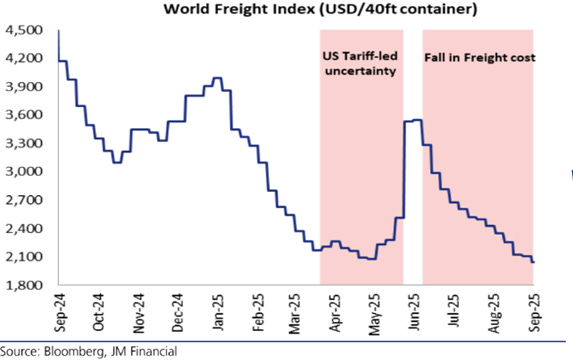

[5] Frieght costs are back to April-lows when tariff uncertainity started…

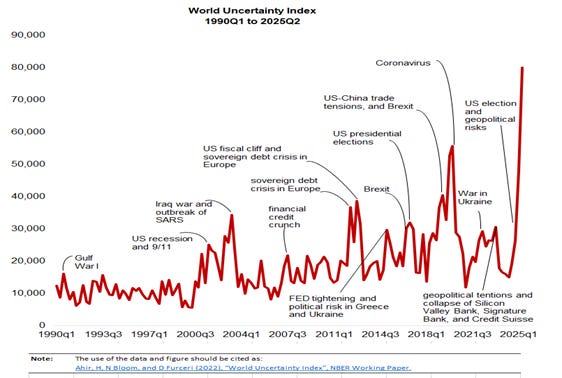

[6] In the past one year, global economic uncertainties have intensified, contributing to a marked slowdown in growth projections—from around 3.2% in 2024 to 2.3–3.0% in 2025—amid persistent disruptions that have eroded investor confidence and trade flows. This volatility stems from a confluence of interconnected factors, including policy unpredictability, deteriorating fiscal positions worldwide, and escalating geopolitical tensions, which collectively amplify risks of financial instability and reduced productivity.

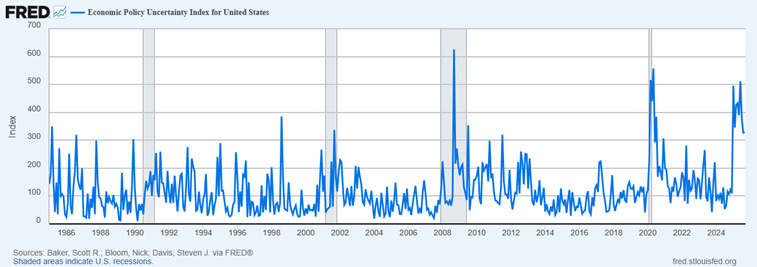

[7] Economic policy uncertainty (EPU) in the US has surged to levels roughly double its long-term average since 2008, exacerbated by the 2024 presidential election and subsequent shifts toward looser regulation, tax cuts, and aggressive tariffs. These US-centric changes have spiked trade policy uncertainty to record highs in early 2025, prompting front-loaded imports and market volatility, while hindering global investment as firms adopt a “wait-and-see” stance.

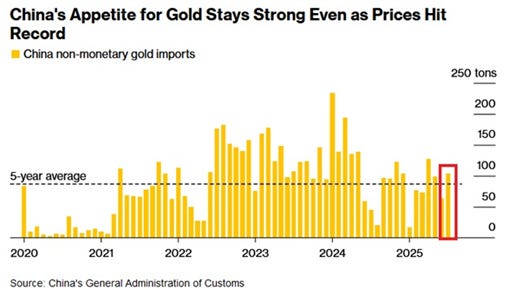

[8] China’s central bank Gold buying remains strong…

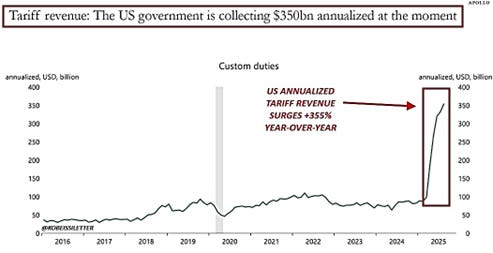

[9] Tariff revenue is holding up well, so far atleast…

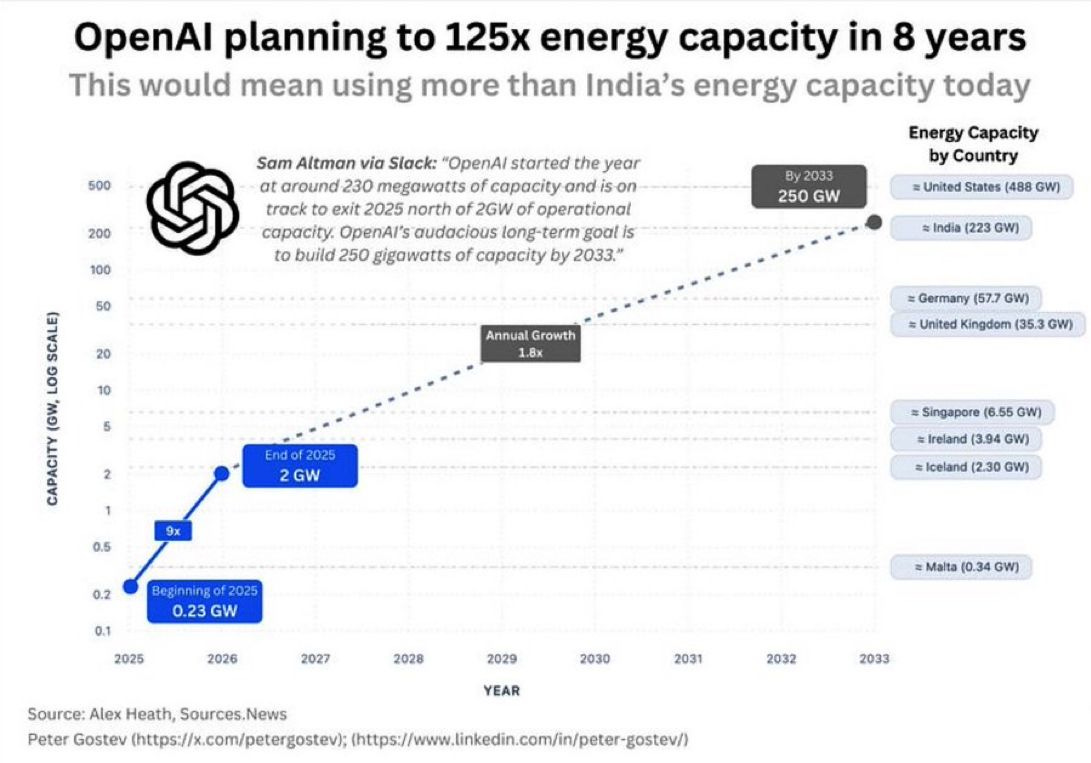

[10] Data centre growth is not going anywhere….

Disclaimer : This newsletter is for information purposes only. In this material, Amit Kumar Gupta (SEBI registered Research Analyst, INH100009327) has used information that is publicly available and is believed to be from reliable sources. While utmost care has been exercised, the author does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers, before acting on any information herein should make their own investigation & seek appropriate professional advice. Any sector(s)/ stock(s)/ issuer(s) mentioned do not constitute any recommendation and the RA may or may not have any future position in these. All opinions/ figures/ charts/ graphs are as on date of publishing (or as at mentioned date) and are subject to change without notice. Any logos used may be trademarks™ or registered® trademarks of their respective holders, our usage does not imply any affiliation with or endorsement by them. Past performance may or may not be sustained in the future and should not be used as a basis for comparison to infer any investment ideas.